Evidence-Based Analysis of Market Dynamics

The LNG market from July 10-31, 2025, exhibited two contrasting movements: price adjustments and rising freight rates occurring simultaneously. A detailed examination of weekly chart data reveals structural changes in progress that exceed market participants’ expectations.

Phased JKM Price Adjustment

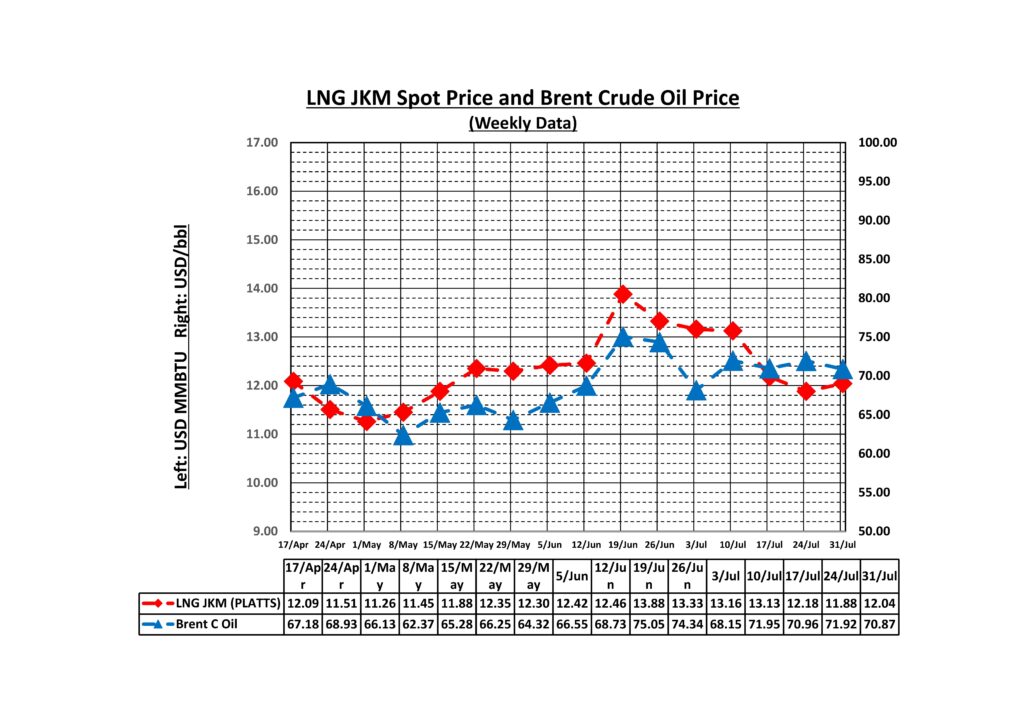

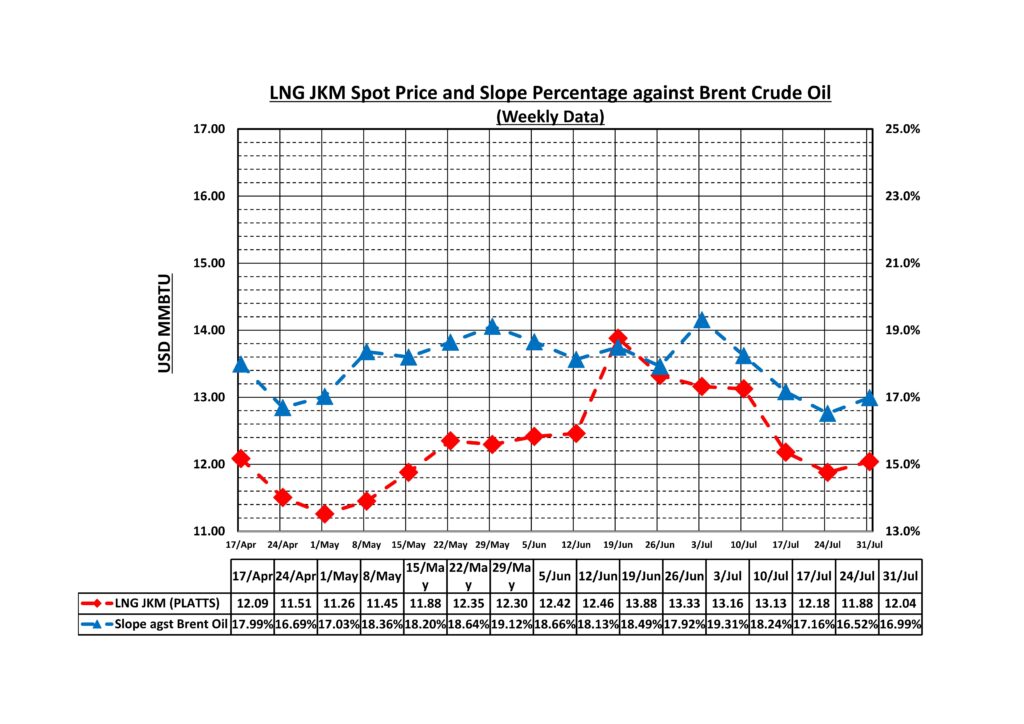

July’s JKM price movement clearly divided into two distinct phases. The first half (July 3-17) saw relatively stable trading from 13.33 to 13.13 USD/MMBtu, reflecting a cautious market stance. However, the latter half (July 17-31) entered a sharp adjustment phase, dropping 8.3% from 13.13 to 12.04 USD/MMBtu.

This adjustment stems from supply-demand easing across major Asian markets. According to JOGMEC reports, JKM fell to “mid-USD 11s/MMBtu” during the July 21-25 week, marking the first return to the USD 11 range since mid-May. Japan’s LNG inventories stood at 1.92 million tonnes as of July 20, up from the previous week, with ample inventory levels suppressing urgent procurement demand.

Notable Freight Rate Uptrend

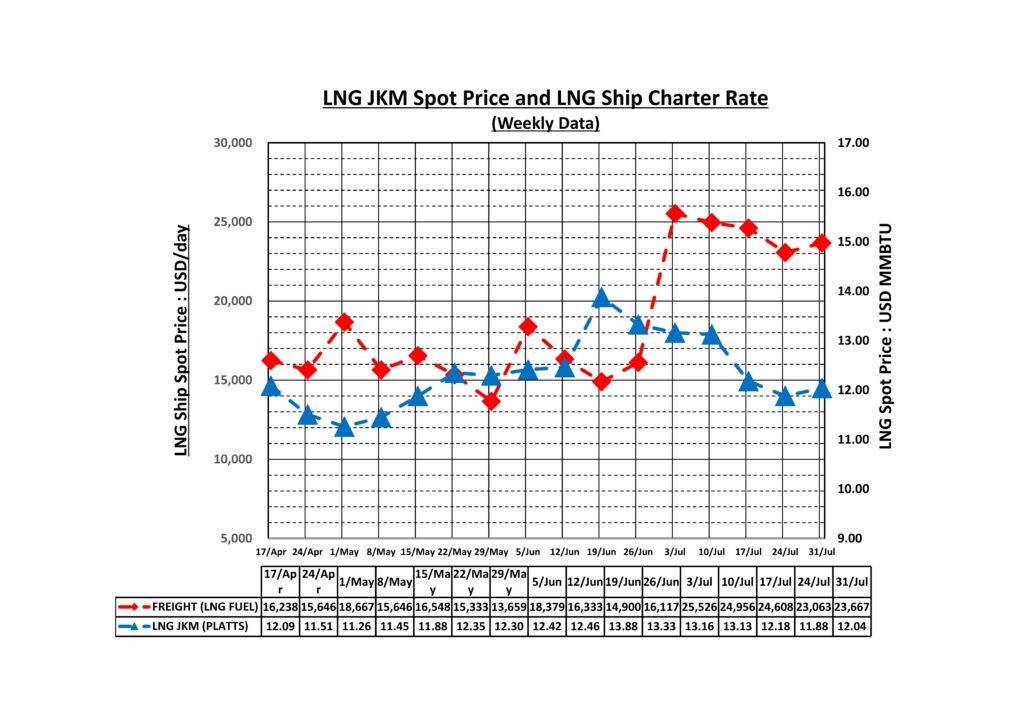

LNG freight rates exhibited a contrasting pattern to JKM prices. Weekly data shows rates rising from 14,900 USD/day on June 19 to 16,117 USD/day on June 26, then surging to 25,526 USD/day on July 3, before settling around 24,956 USD/day (July 10), 24,608 USD/day (July 17), 23,063 USD/day (July 24), and 23,667 USD/day (July 31).

Particularly noteworthy is the sharp spike from June 26 to July 3, representing a 58.4% increase from 16,117 to 25,526 USD/day. This is analyzed as a market reaction to heightened geopolitical risks. Throughout July, rates remained elevated around 25,000 USD/day, indicating the establishment of a persistent transportation risk premium.

Evolving JKM-Brent Correlation

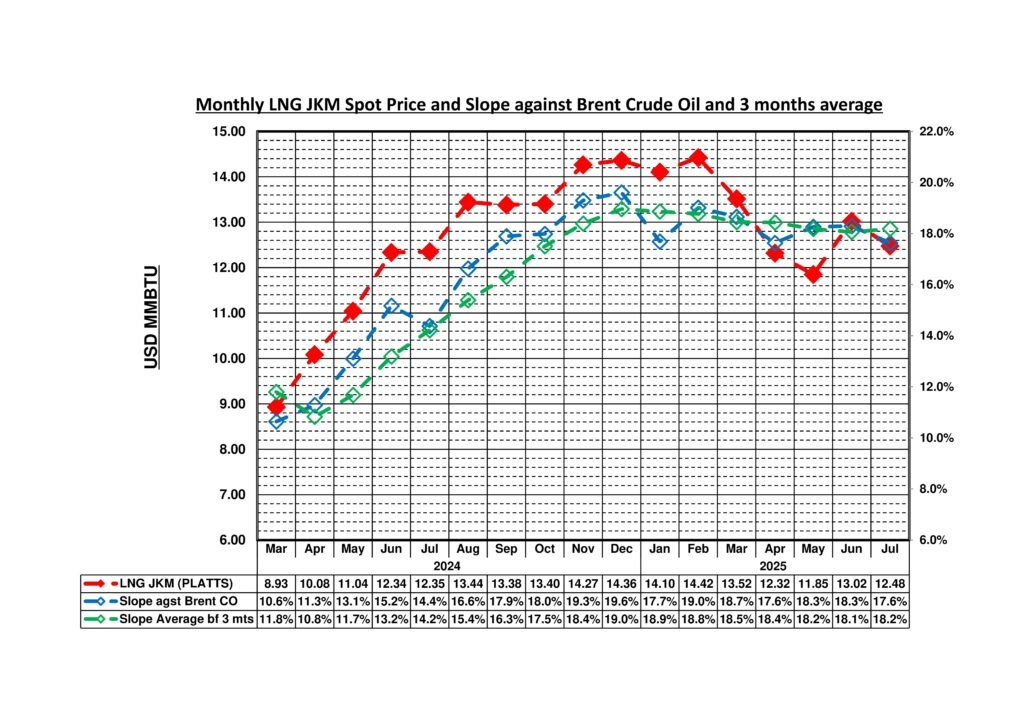

The relationship between JKM and Brent crude shows interesting developments. During the first half of July, when Brent prices plunged from 74.34 to 68.15 USD/bbl, JKM maintained relative stability, causing the Slope ratio to temporarily rise to 19.31%. However, as JKM entered adjustment mode in the latter half of July, the Slope ratio declined to 16.99%, positioning at the lower bound of the appropriate range.

This movement suggests that the LNG market is gradually gaining independence from mechanical crude oil linkage, responding more strongly to Asia-specific supply-demand factors. The month-end Slope ratio of 16.99% falls below historical average levels, indicating LNG’s relative value proposition.

Dual Nature of Geopolitical Factors

Geopolitical risks are exerting dual influences on the market. On one hand, Middle East tensions have clearly added risk premiums to freight rates. The freight surge from late June to early July directly reflects these geopolitical risks.

Conversely, LNG prices themselves have shown only limited responses to geopolitical risks. While there was temporary price elevation during the mid-June Israel-Iran conflict, July saw adjustments prioritizing supply-demand fundamentals. This demonstrates that market participants have improved their adaptability to geopolitical shocks.

Changing Seasonal Patterns

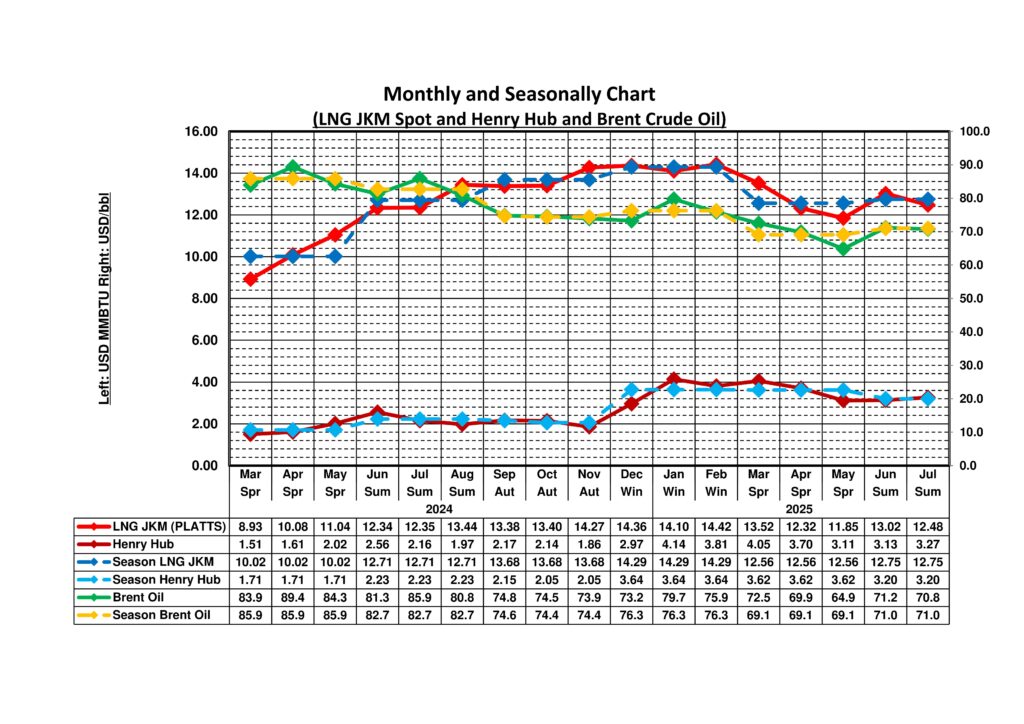

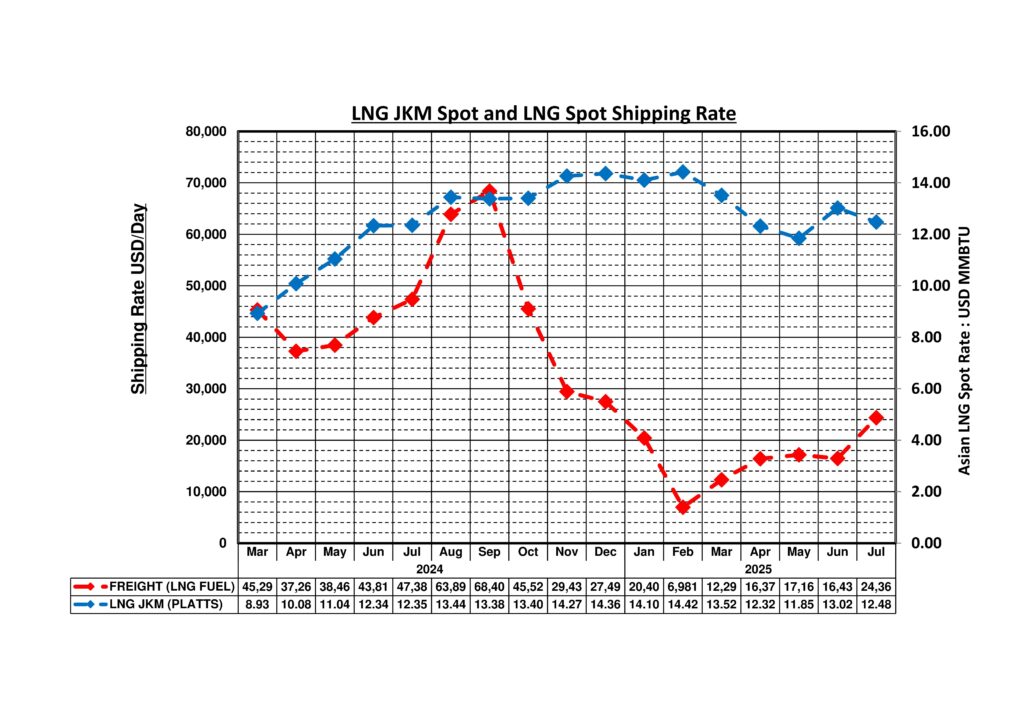

Traditionally, July represents the seasonal demand trough in LNG markets, with both prices and freight rates typically reaching annual lows. However, July 2025 presented an unusual scenario where JKM prices adjusted while freight rates maintained elevated levels.

This deviation from seasonality reflects the normalization of geopolitical risks and structural changes in transportation markets. Procurement strategies dependent on traditional seasonality require revision, emphasizing the growing importance of year-round risk management.

Strategic Implications of Market Structural Changes

These analyses reveal that the LNG market is gradually diverging from previously predictable patterns, evolving into a more complex and multifaceted marketplace. While supply-demand fundamentals maintain dominance in price formation, freight rates now permanently incorporate geopolitical risks, creating a new dual structure.

This dual structure demands more sophisticated risk management capabilities from market participants than ever before. The transition from simple seasonal procurement to dynamic procurement strategies that constantly consider geopolitical risks has become urgent. The July 2025 market dynamics clearly demonstrate that the LNG industry has entered a full-scale adaptation period to a new market environment.

Leave a Reply