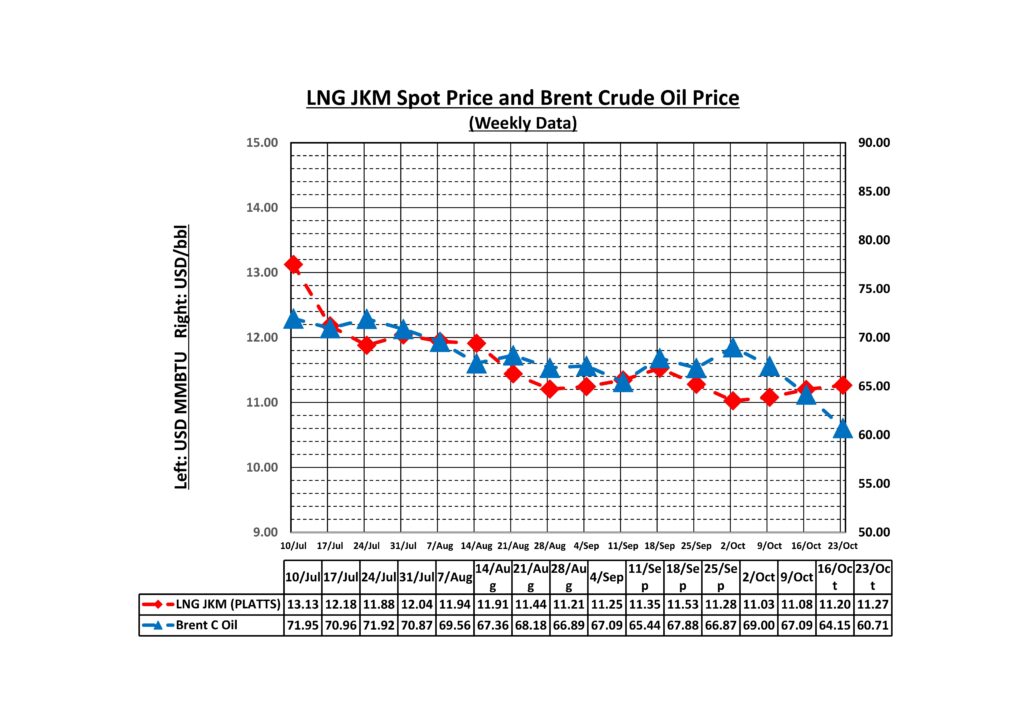

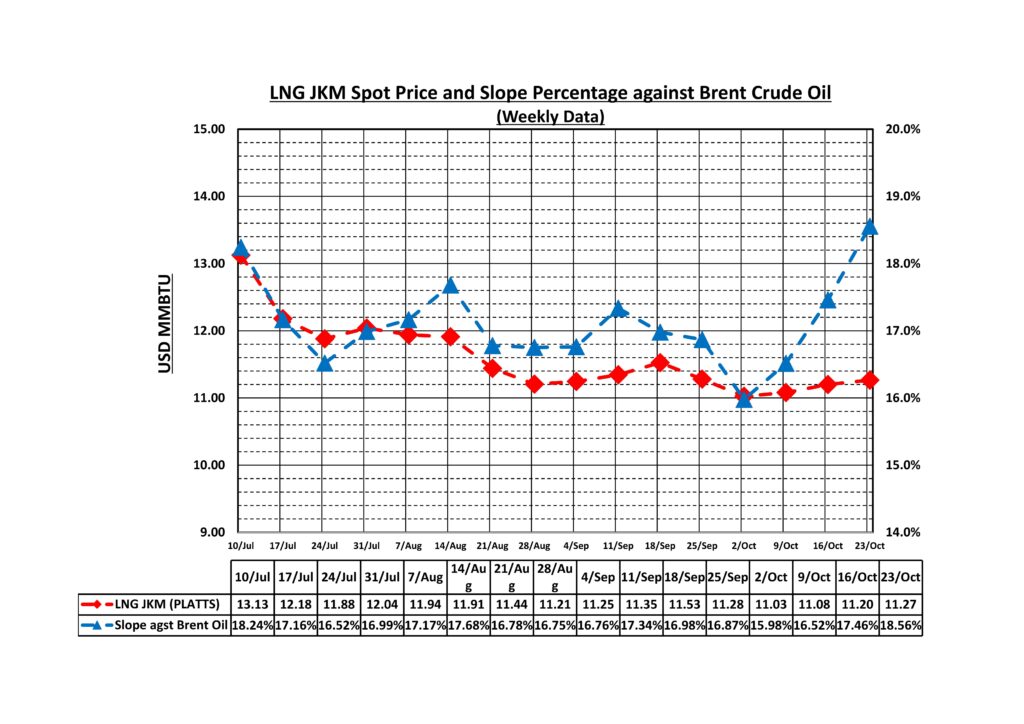

1. Emergence of Price Asymmetry

During the four weeks from September 25 to October 23, JKM spot prices remained stable at approximately $11.27/MMBtu, while Brent crude declined by 9.2% and LNG shipping rates fell by 14.4%, revealing an asymmetric price trajectory. This asymmetry demonstrates that the LNG market is structurally decoupling from its traditional correlation with crude oil prices. The Slope ratio increased from 16.87% in the previous month to 18.56%, indicating that market mechanisms enabled JKM prices to maintain relative strength even during a period of declining oil prices.

2. Factors Behind Brent Crude Price Decline

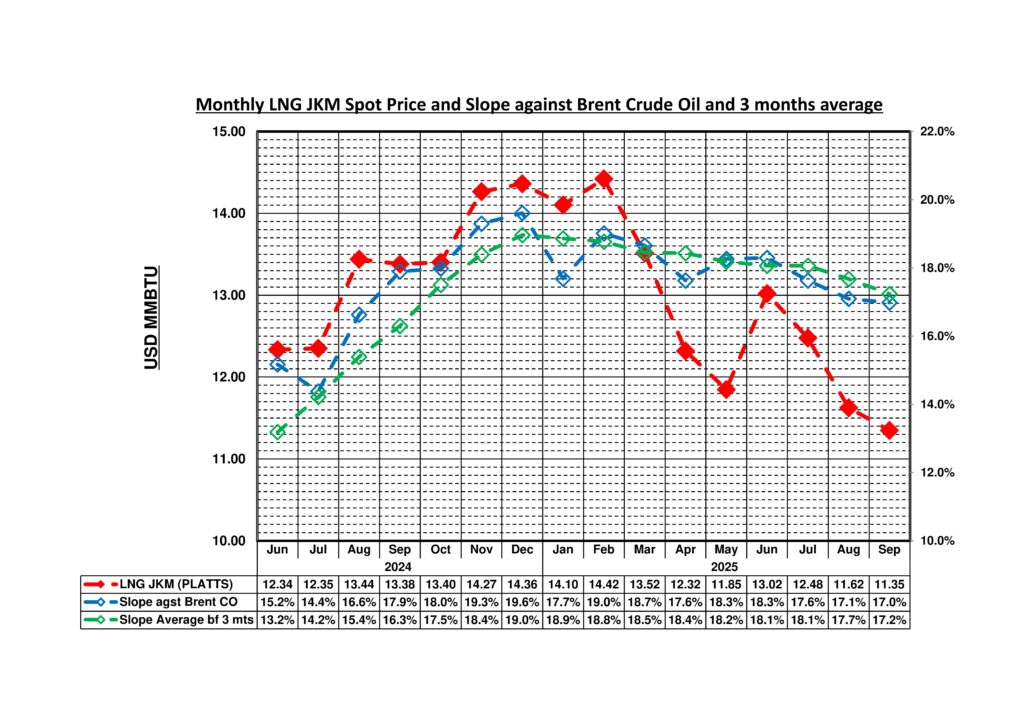

Brent crude declined from approximately $72.60/barrel on September 25 to $65.94/barrel on October 23. According to the EIA’s October 2025 Short-Term Energy Outlook (STEO), this decline stems from a global supply surplus, with crude oil production exceeding demand. The EIA forecasts average Brent prices of $62/barrel in Q4 2025, falling to $52/barrel in 2026, as inventory buildup creates downward price pressure.

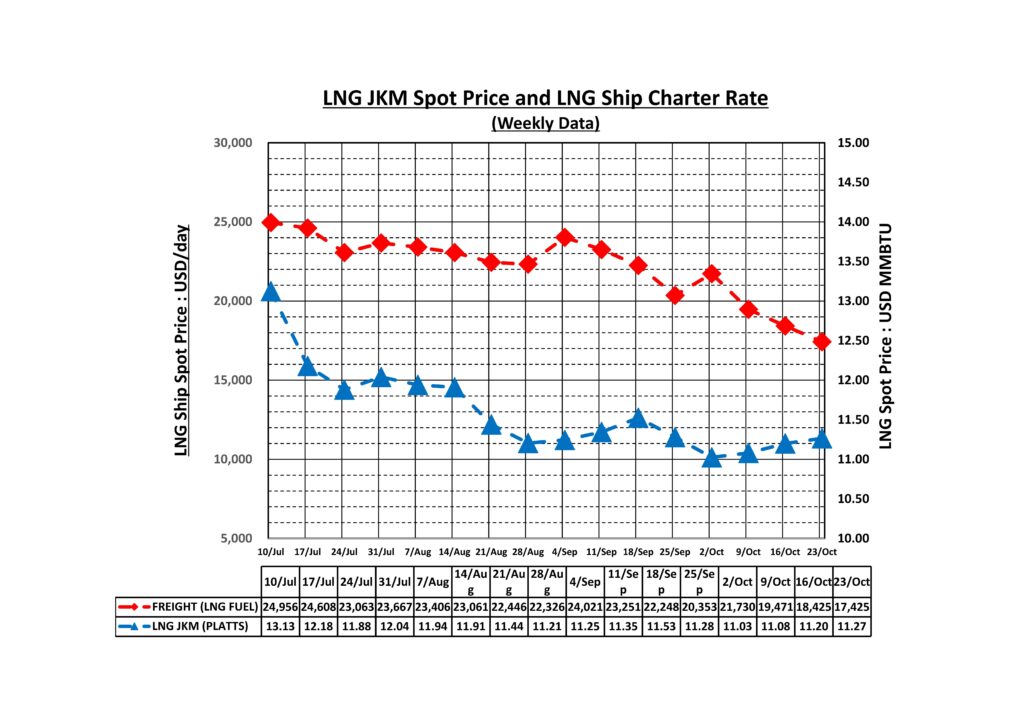

3. Primary Driver of LNG Shipping Rate Decline: Correlation with Oil Prices

LNG shipping rates declined 14.4% from their July peak of $25,526/day to $17,425/day on October 23. The primary driver of this decline is the correlation with the 9.2% drop in Brent crude prices. In the shipping industry, fuel costs account for the majority of operational expenses, and declining oil prices directly reduce shipping costs. Additionally, the large influx of new LNG carriers entering service in 2025 has eased vessel supply-demand dynamics, with spot charter rates hitting record lows in Q1 2025. Although diversions via the Cape of Good Hope route (20% longer distance) continue due to Red Sea instability, the fuel cost savings from lower oil prices have offset this impact.

4. Factors Supporting JKM Price Stability

JKM prices maintained stability around $11.27/MMBtu due to the following supply-demand balance. On the supply side, continuous deliveries from diverse sources, including Qatar, Australia, Malaysia, Russia, and the United States, were secured. On the demand side, Europe continued inventory build-up in preparation for the Ukraine situation, while robust demand from China and India in Asian markets provided underlying support. Particularly in Europe, natural gas inventories reached levels 5% above the five-year average as of October 2025, with procurement for winter demand largely completed, suppressing upward price pressure.

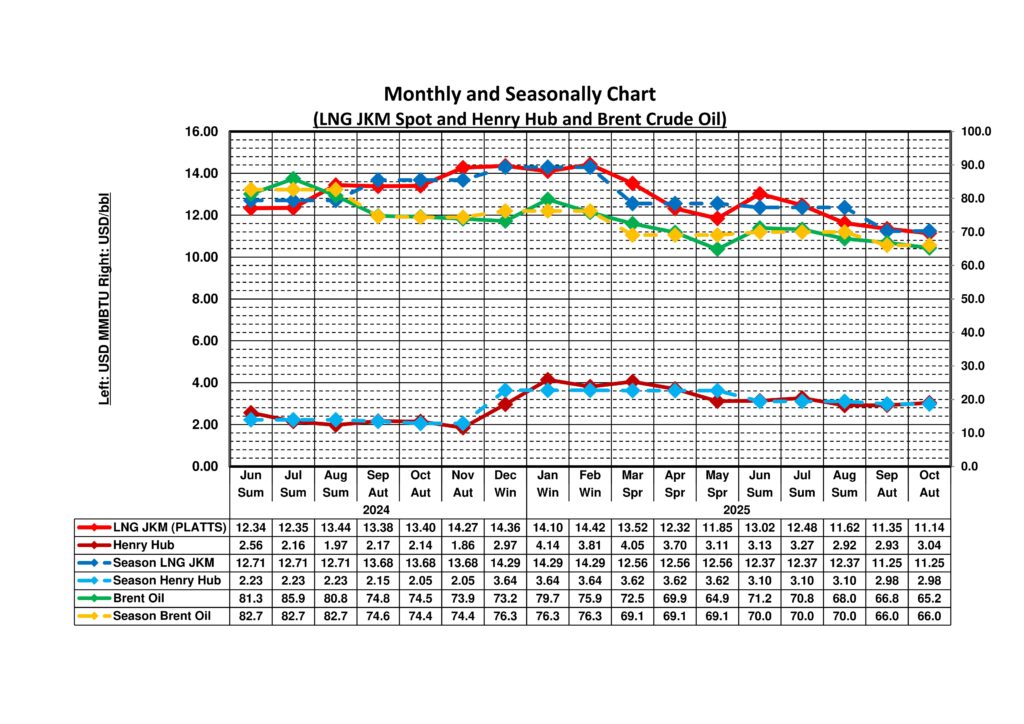

5. Numerical Evidence for Henry Hub Price Surge

Henry Hub spot prices surged 18.8% from $2.56/MMBtu in September to $3.04/MMBtu in October. According to the EIA’s October 2025 STEO, U.S. natural gas demand is projected to average 91.5 Bcf/day in 2025, reaching a record high with annual growth of 4-6% compared to 2024. LNG exports reached 15.1 Bcf/day in September, setting a new record 11% above the previous peak of 13.6 Bcf/day in December 2023. Venture Global’s Plaquemines LNG facility supplied 1.6 million tons per month (17% of total U.S. exports) as of August. As of the second week of October, LNG export feedgas reached 16.5 Bcf/day, up 27.3% year-over-year. Natural gas inventories stood at 3,808 Bcf as of October 17, which is ample; however, market participants increased futures buying after AccuWeather forecast the 2025-2026 winter to be “normal to above-normal cold.” The EIA projects Henry Hub prices will rise to $4.10/MMBtu by January 2026.

6. Current Geopolitical Assessment (as of October 27, 2025)

As of late October 2025, the Middle East geopolitical environment is characterised by the following conditions. Airstrikes against Hezbollah positions continue across Lebanon in Israeli-Lebanese operations, with ceasefire negotiations showing no progress. Iran issued warnings of retaliation against Israel on October 26, keeping tensions elevated. In Gaza, although a ceasefire agreement took effect on October 9, sporadic attacks continue and the ceasefire’s sustainability remains fragile. In the Red Sea, over 190 Houthi attacks have not completely subsided, with the potential for renewed Israeli-Houthi conflict being noted.

Impact on Energy Markets:

At present, Middle East tensions have not reached a level that would cause direct LNG supply disruptions. However, instability in Red Sea routes persists, forcing LNG carriers to continue diversions via the Cape of Good Hope. Should military escalation between Iran and Israel occur, concerns exist regarding LNG supplies via the Strait of Hormuz (Qatari LNG, etc.). However, no concrete supply constraints have materialised as of October.

7. Future Outlook

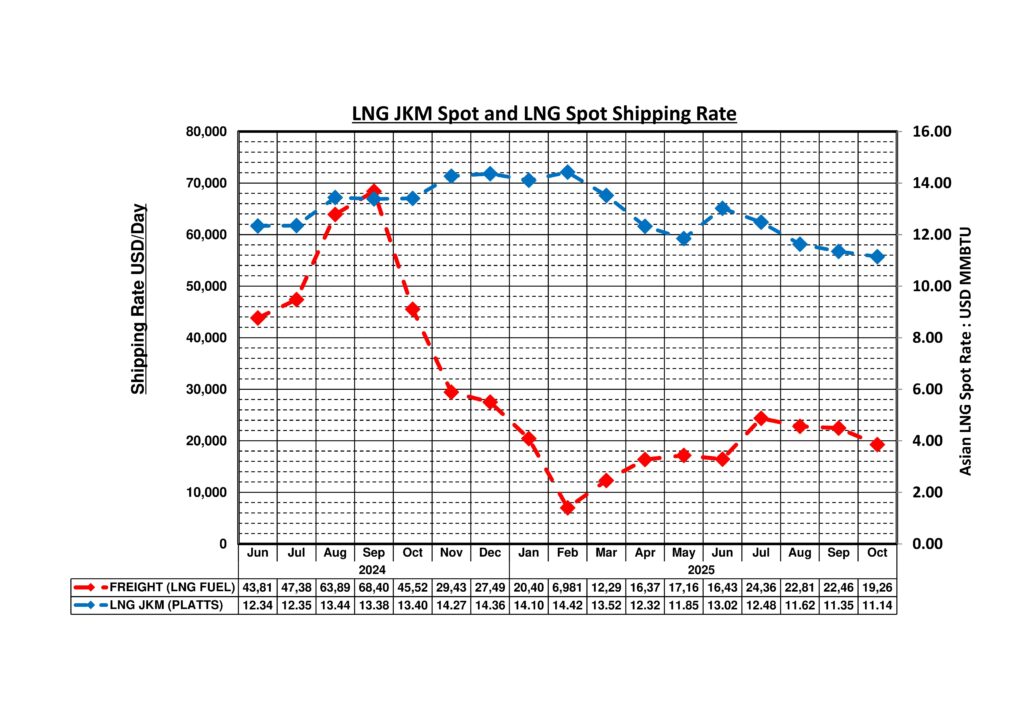

The LNG market going forward will be dominated by the tug-of-war between supply expansion and demand uncertainty in price formation. U.S. LNG export capacity will expand to 16.3 Bcf/day by 2026, with Plaquemines LNG Phase 2, Golden Pass LNG, and others coming online. The IEA forecasts global LNG supply growth of 7% (40 bcm) in 2026, representing the largest supply increase since 2019. According to the Discovery Alert analysis, supply surplus is projected to reach approximately 50 bcm in 2026 and 200 bcm by 2030.

Downside risks exist on the demand side. Chinese LNG imports declined by over 20% year-over-year in the first half of 2025, and Asia’s overall demand growth rate fell to its lowest level since 2022 amid elevated prices. In Europe, gas demand is forecast to peak in 2025, with a declining trend projected through 2030 (IEEFA).

As a result, a paradoxical divergence between Henry Hub and JKM prices may emerge. In the U.S. domestic market, the convergence of increased LNG exports, data centre demand, and winter demand is expected to push Henry Hub prices up to $4.20-4.30/MMBtu in 2026 (EIA and NAGA forecasts). Meanwhile, in the global LNG market, supply surplus is expected to keep JKM prices around $11/MMBtu or create downward pressure in 2026 (GECF forecast).

Middle East geopolitical risks remain a factor in price volatility. Should military conflict between Iran and Israel escalate or the Strait of Hormuz be blockaded, temporary price spikes are possible due to concerns over Qatari LNG supply. However, under conditions of structural supply surplus, geopolitical premiums are likely to remain limited and temporary. Beyond 2026, supply surplus will become the dominant theme in LNG markets, with upside potential for JKM prices structurally constrained.

Leave a Reply